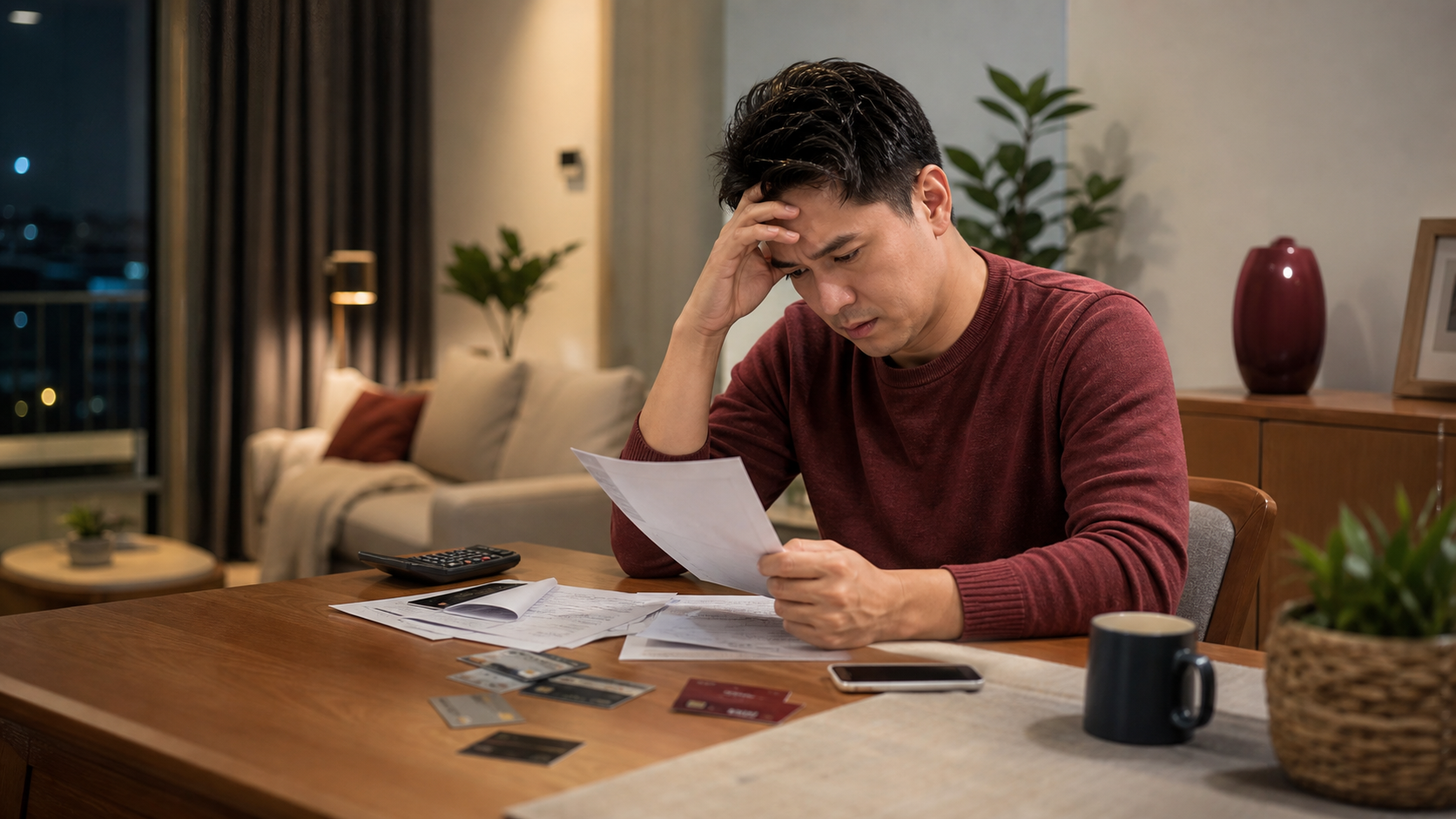

Debt letters, AKPK decisions, and bankruptcy risk made clear.

PWVH helps Malaysians understand urgent debt letters, pre-AKPK options, personal bankruptcy risk, and company winding-up pressure before the next deadline passes.

What do you need help with?

Pick a group below, or scroll down to see everything.

Urgent Letters

Guides for letters of demand, court papers, bankruptcy notices, winding-up notices, bank recall, and auction pressure.

View allPersonal Debt

Guides for individuals facing credit card debt, personal loans, housing arrears, guarantor risk, and pre-AKPK decisions.

View allBusiness Debt

Guides for company letters, SDRS, supplier debt, director personal guarantees, cash-flow pressure, and restructuring.

View allWho We Help

Situation pages for salary earners, homeowners, guarantors, directors, SME owners, and self-employed borrowers.

View allUrgent Letters

Guides for letters of demand, court papers, bankruptcy notices, winding-up notices, bank recall, and auction pressure.

Letter of Demand

A letter of demand is a warning stage. Review the sender, amount, deadline, documents, and whether negotiation or legal advice is needed before the matter escalates.

See how

Court Summons or Judgment Debt

Court documents are different from ordinary reminder letters. Confirm what has been filed, the hearing or response date, and whether you need a lawyer immediately.

See how

Bankruptcy Notice

A bankruptcy notice is serious because non-compliance can become an act of bankruptcy. The Malaysian courts guide states the notice demands payment within 7 days from service and is valid for 3 months.

See how

Company Winding-Up Notice

Company winding-up is different from personal bankruptcy. SSM guidance explains that Section 466 notices can lead to winding-up action if a company fails to comply within the demand period and the debt threshold is met.

See how

Bank Recall or Auction Risk

Bank recall and auction risk need fast document review because property, hire purchase, and secured facilities each follow different paths.

See howPersonal Debt

Guides for individuals facing credit card debt, personal loans, housing arrears, guarantor risk, and pre-AKPK decisions.

Before AKPK Review

Before approaching AKPK, organize your debts, income, arrears, legal letters, and affordability so the discussion is clearer.

See how

AKPK Debt Management Programme

AKPK DMP is an official repayment-plan route for eligible individuals. PWVH can help you understand what information to prepare before you apply directly.

See howPersonal Bankruptcy Process Malaysia

Personal bankruptcy commonly moves from judgment debt to bankruptcy notice, act of bankruptcy, creditor petition, and bankruptcy order if legal requirements are met.

See how

Credit Card Debt

Review all card balances, interest pressure, legal letters, and affordability before choosing AKPK, consolidation, settlement, or creditor negotiation.

See how

Personal Loan Debt

A personal-loan review should compare settlement, restructuring, AKPK, refinance, or creditor negotiation only after affordability is clear.

See how

Guarantor Risk

Guarantor cases need fast review of the guarantee document, debtor status, demand letter, and whether personal bankruptcy exposure exists.

See howBusiness Debt

Guides for company letters, SDRS, supplier debt, director personal guarantees, cash-flow pressure, and restructuring.

Company Letter of Demand

Company letters should be reviewed for registered office service, amount, creditor type, personal guarantee exposure, and winding-up risk.

See how

AKPK SDRS for SME Debt

AKPK SDRS is an official route for viable SMEs facing difficulty servicing debt with financial institutions. It is separate from ordinary supplier negotiation.

See howCompany Winding-Up Process Malaysia

For inability-to-pay-debts cases, Section 466 notice pressure can lead to a winding-up petition if the company does not act and the prescribed threshold is met.

See how

Director Personal Guarantee

A director personal guarantee can create personal exposure even when the original borrower is the company. Review it before negotiation.

See howCreditor Negotiation

Negotiation is stronger when you know what you can pay, what you can prove, and what the creditor may do next.

See how

Business Cash-Flow Problems

Cash-flow distress needs a route map across bank debt, trade creditors, statutory arrears, and director exposure before one creditor controls the timeline.

See howWho We Help

Situation pages for salary earners, homeowners, guarantors, directors, SME owners, and self-employed borrowers.

Individuals & Salary Earners

We help organize personal debt, legal letters, AKPK readiness, and affordability before you make the next promise to creditors.

See how

Business Owners & Directors

We help directors separate company exposure, personal exposure, and urgent creditor timelines.

See howGuarantors

We help you organize guarantee documents, creditor letters, and the possible personal-risk route.

See how

Self-Employed Borrowers

Self-employed debt reviews need bank statements, real cash-flow, creditor timelines, and a payment plan built around actual income.

See howSimple help you can trust.

- We separate personal bankruptcy risk from company winding-up pressure.

- We explain official routes such as AKPK DMP, AKPK SDRS, and MdI in plain language.

- We do not pretend to be AKPK, a bank, a law firm, or a guaranteed debt cancellation service.

- We focus on the period before the problem escalates, when preparation still matters.

Just say hi. We'll help you figure it out.

Fill in the short form first so we can capture your inquiry and follow up on WhatsApp.

Chat on WhatsApp